What Lenders Look For Before Pre-Approval in Arizona

If you are thinking about buying a home in Arizona, pre-approval is the step everyone talks about but few people actually understand.

Most first-time buyers assume pre-approval is a quick yes or no.

In reality, lenders are evaluating a full financial picture, especially for buyers shopping in places like Mesa and the East Valley.

This guide explains what lenders actually look for before issuing a pre-approval in Arizona, so you can prepare without stress or surprises.

Why Pre-Approval Matters So Much in Arizona

In Arizona, pre-approval is not optional.

Sellers expect it.

Builders require it.

Offers without it are rarely taken seriously.

Pre-approval tells everyone involved:

-

You are financially vetted

-

Your numbers are realistic

-

The deal has a strong chance of closing

It also protects you from falling in love with homes that do not fit your budget.

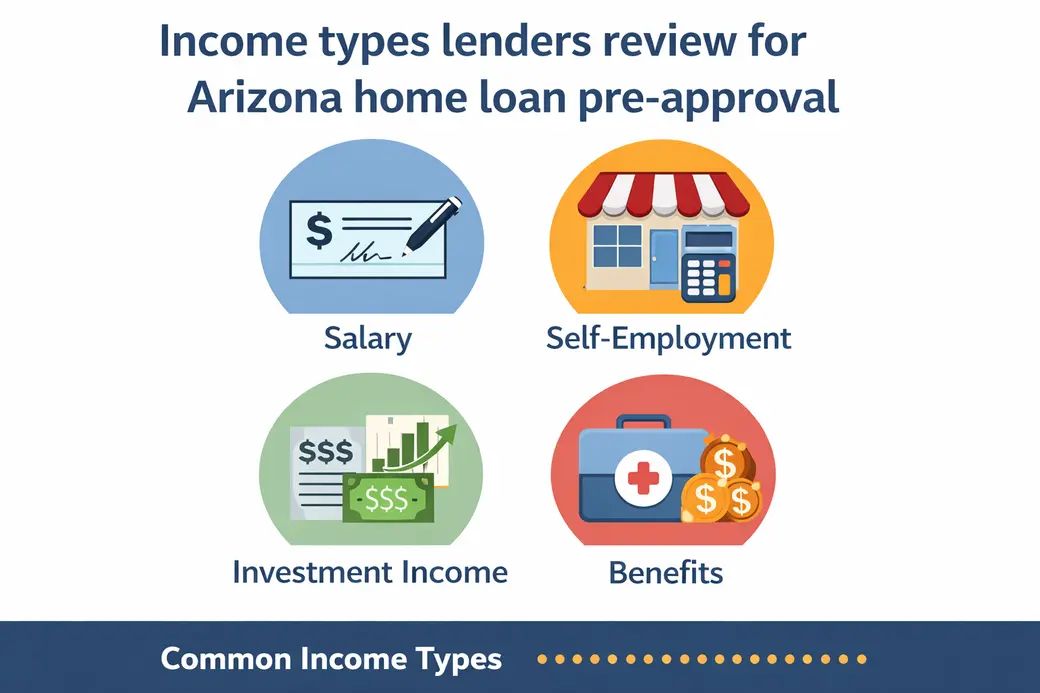

Income: Stability Over Perfection

Lenders care more about consistency than perfection.

They look for:

-

Stable employment history

-

Reliable income sources

-

Documentation that supports what you earn

This applies whether you are:

-

Salaried

-

Hourly

-

Self-employed

-

Commission-based

Changing jobs does not automatically hurt you, especially if you stayed in the same field. What matters is how predictable your income appears on paper.

Credit: More Than Just the Score

Credit scores matter, but they are not the whole story.

Lenders also review:

-

Payment history

-

Credit utilization

-

Types of accounts

-

Recent inquiries

Many first-time buyers in Mesa assume one late payment disqualifies them. That is rarely true.

What raises concern is:

-

Repeated late payments

-

Maxed-out credit cards

-

Recent large credit changes

Small improvements before pre-approval can make a noticeable difference.

Debt-to-Income Ratio: The Quiet Deal Breaker

Debt-to-income ratio, often called DTI, is one of the biggest factors lenders evaluate.

DTI compares:

-

Monthly debt payments

-

Gross monthly income

This includes:

-

Car loans

-

Student loans

-

Credit cards

-

Personal loans

Many buyers focus only on their credit score and forget this piece entirely.

Reducing monthly debt can sometimes help more than increasing income.

Assets: What You Have Available

Assets are about access, not just savings.

Lenders look at:

-

Checking and savings accounts

-

Retirement funds if applicable

-

Gift funds when allowed

They want to confirm:

-

You can cover your down payment

-

You can handle closing costs

-

You have some reserves left over

Draining every account to buy a home is rarely ideal, even if it is technically allowed.

Documentation: The Part Buyers Underestimate

This is where many buyers feel overwhelmed.

Lenders typically request:

-

Pay stubs

-

W-2s or tax returns

-

Bank statements

-

Identification

The goal is not to interrogate you.

The goal is to verify consistency and accuracy.

Providing documents early and clearly can speed up the entire process.

Employment Gaps and Life Changes

Arizona lenders understand real life happens.

They will ask about:

-

Employment gaps

-

Career changes

-

Recent relocations

This is especially common for buyers moving to the East Valley from out of state or transitioning roles.

Clear explanations matter more than avoiding the conversation.

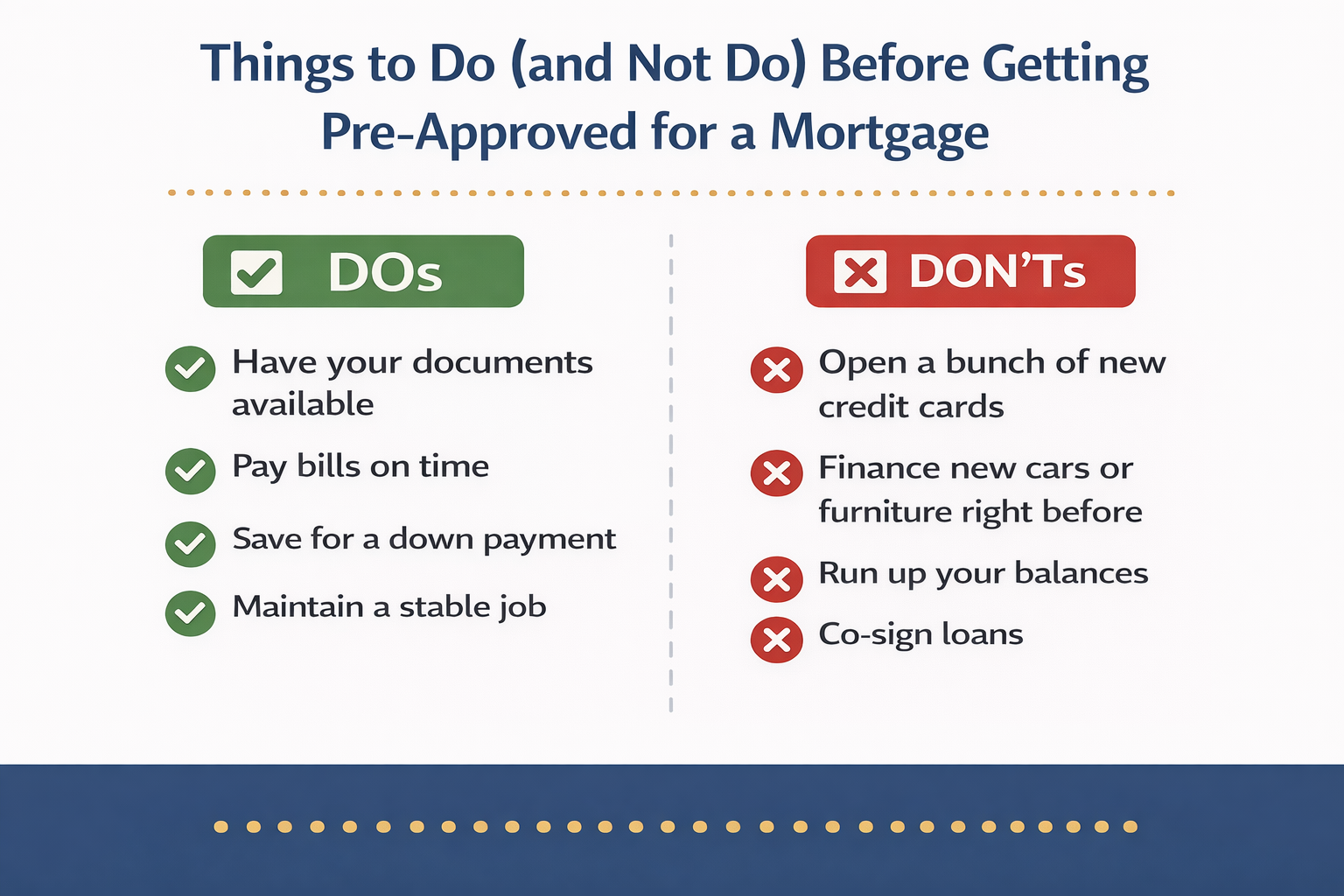

Credit Activity Before Pre-Approval

This part trips buyers up more than it should.

Before pre-approval, avoid:

-

Opening new credit accounts

-

Financing furniture or cars

-

Running up balances

-

Co-signing loans

Even small changes can affect your approval amount or loan terms.

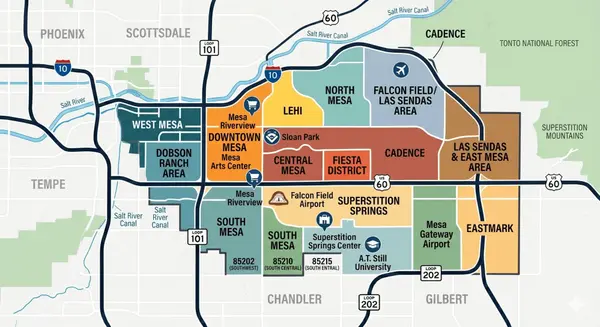

How This Varies by Area and Loan Type

What lenders look for does not change by city, but the price points do.

Buyers shopping in Gilbert, Queen Creek, or San Tan Valley may see:

-

Different qualifying ranges

-

Different cash expectations

-

Different competition levels

Loan type also plays a role. FHA, conventional, and VA loans each evaluate risk slightly differently.

What Buyers Should Focus On Before Applying

Instead of trying to be perfect, focus on being prepared.

Helpful steps include:

-

Reviewing your credit report

-

Organizing documents early

-

Understanding your monthly comfort zone

-

Asking questions before applying

Pre-approval should feel clarifying, not intimidating.

Frequently Asked Questions About Pre-Approval in Arizona

Does pre-approval guarantee I can buy a home?

No. It confirms eligibility at a point in time. Final approval happens later after inspections and appraisal.

How long does a pre-approval last?

Most Arizona pre-approvals are valid for about 60 to 90 days, depending on the lender.

Can I get pre-approved before choosing a neighborhood?

Yes. Many buyers get pre-approved first, then narrow areas like Mesa or nearby cities afterward.

Will checking my credit hurt my score?

A single mortgage inquiry typically has minimal impact compared to ongoing credit activity.

Should I talk to a lender even if I am not ready yet?

Yes. Early conversations help you plan and avoid surprises later.

Final Thoughts on Pre-Approval in Arizona

Pre-approval is not about judgment.

It is about clarity.

Once you understand what lenders look for, you can approach the process with confidence instead of fear.

If you want access to pre-approval checklists, lender resources, or Arizona-specific buyer tools, you can explore the free resources available on my site

Thinking about buying a home in Arizona? Download my free First Time Buyer Guide and get clarity before you make your first move. Click here to grab your free guide

Categories

Recent Posts

"Real estate isn’t just about buying and selling houses—it’s about creating opportunities, building wealth, and turning dreams into reality. Everyone deserves a place to call home, and I’m here to make that happen."